The Global Digital Outlook Study from Forrester and SoDA collects data on spending trends, the adoption of emerging technology, perspectives on the future of digital and evolving priorities of both brand marketers and agency leaders.

The Global Digital Outlook Study from Forrester and SoDA collects data on spending trends, the adoption of emerging technology, perspectives on the future of digital and evolving priorities of both brand marketers and agency leaders.

There are some very interesting insights both from the client and the agency sides.

Good news is, confidence is high, investments in digital continue to increase, the role of design and creative remain the most important, agency models are continueing to change and speed and agility remain vital.

This years report highlights the following trends:

- BIGGER PIE… AND MORE HUNGRY MOUTHS AT THE TABLE

The 2019 Digital Outlook finds a majority of agency leaders optimistic about the future even as they remain clear-eyed about the challenges facing their businesses. Despite all the doom and gloom regarding broken agency models (vivid images of fire, brimstone and post-apocalyptic demogorgans come to mind), agency leaders are reporting healthy performance in 2018 and a solid outlook for 2019. More than half of agency leaders reported growth in revenue and total profit in 2018 (56% and 55% respectively) and 79% said they are confident that the next 12 months will be even stronger in terms of profitable growth.

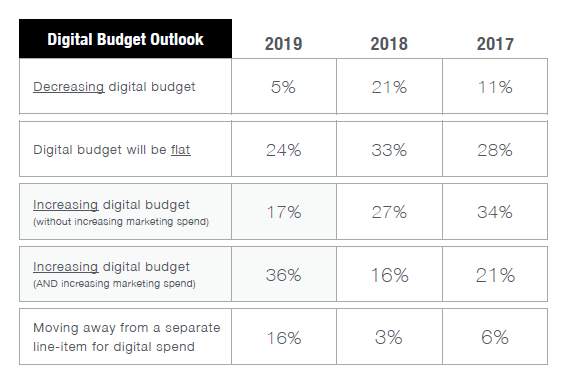

Confidence levels are bolstered (and, perhaps, justified) by a strong spending outlook from client-side marketing leaders: 53% plan to increase their digital spend in 2019 and 36% plan to increase overall marketing spend. More importantly, 43% plan to increase their spending with external agency partners making this one of the strongest outlooks we’ve seen since we began tracking in 2013.

2. BATTLE ROYALE OR TOKYO DRIFT TO THE MIDDLE?

The marketing world has been obsessed with the incursion of management and IT consultancies into the sacred creative territory of agencies. Too much of the industry commentary, however, adopts a binary view on the matter suggesting that only one model will prevail in this battle royale between consultancies and holding companies.

This is a simplistic assessment for a complicated and interconnected ecosystem of digital providers of all shapes, sizes and flavors. It also tends to ignore a vast swath of the independent (and innovative) agency market less obsessed with global scale and wall street valuations. While our data this year revealed a 24-point decline in marketers’ openness to using consultancies for digital agency assignments (53% said they were “Very Open” or “Open” this year vs. 77% in 2017), we continue to see an array of partner types tackling digital initiatives.

3. AGENCIES PRACTICE MIXED MODEL ARTS

Our findings this year point to an active evolution of the agency business model with some moving towards specialization while others seek to expand the breadth of their influence with new capabilities. An astounding 61% of agency leaders this year said they were actively re-evaluating their core business model. Experimentation with different pricing models (26%), going to market with 3rd party partners to round out service offerings (25%), and deeper collaboration/integration with their clients’ other partners (30%) are just a few of the directions under exploration. On the capabilities front, agency leaders point to areas such as strategy, data, platforms and technology as key areas for revenue growth in 2019. Interestingly, these capabilities are traditional strongholds for the consultancies and we expect the competitive battleground to expand.

Many native digital agencies, traditional integrated agencies and consultancies are racing towards a melee at the center of the marketing and customer experience ecosystem. It’s also clear that new areas of specialization have emerged. For instance, more than 30% of all agency respondents said they do not currently offer any services related to voice-based applications, AI-driven digital experiences or experiential installations that blend physical and digital environments. We also see agency leaders tackling a new and unique mix of capabilities across the digital marketing and experience value chain. S4 Capital’s strategy to combine global production, content, data and media into a new integrated entity is one such example of the mixed models beginning to emerge.

4. SPEED, VALUE, AGILITY AND TRANSPARENCY

Speed. 56% of agency leaders said that speed of delivery is becoming a bigger factor in whether or not they win new projects and 63% of client-side marketing leaders said that producing and publishing personalized digital content, more quickly, is a major priority for their business.

Agility. Flexibility and agility are cornerstones of collaboration. Client-side marketing leaders point to “more flexible/nimble working models” as one of the top areas of improvement they’d like to see from their agency partners. On the other side, agency leaders say that “working directly with clients’ other partners in a more collaborative, integrated way” is one of the top ways in which their typical engagement models are changing. Additionally, more than 60% of all respondents agree that the in-sourcing of digital capabilities is having major impact on the way clients and agencies now partner.

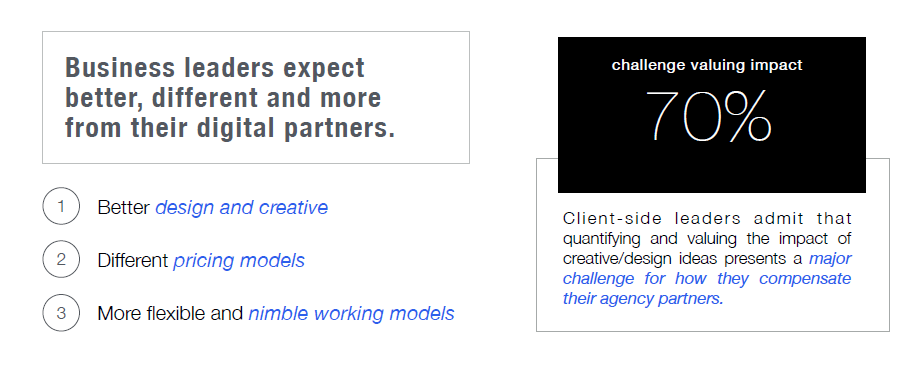

Value. Client-side marketing leaders ranked “different pricing models” as one of the top changes they’d like to see from their agency partners and pointed to “pricing/value” as the top reason they typically terminate a partner relationship. Agency leaders seem to be begrudgingly concede the point, ranking “pricing/value” the second highest reason for why they are typically terminated by their clients. Additionally, a whopping 70% of client-side marketers admit that properly quantifying and valuing the impact of creative ideas represents a major challenge for how they compensate their agency partners.

Transparency. 66% of client-side marketing leaders said they are demanding greater detail and transparency in how their agency partners track and report on budget spending. While not quite as high, 50% of agency leaders agreed and said that their clients are increasingly demanding greater detail and transparency.

So what does this all mean? Bedrock elements of the agency business (creative and innovation) are still top of mind for clients. In fact, “Better Design / Creative” is the number one improvement they’d like to see from their agencies. But there are many paths to success and given the growing realities of operating in an multi-partner ecosystem (often with in-house teams in the mix), greater scrutiny for CMO’s entrusted with more responsibility and bigger budgets, and market pressure to move quickly, we see business leaders placing a bigger premium on the working models of the partners they select and with a keen eye towards if/how/where they can be a collaborative, nimble and efficient element in the overall ecosystem.

5. CREATIVE LEADERS GAIN CURRENCY IN THE C-SUITE

The creative discipline has historically been confined to the marketing function and deployed as an adjunct to business or product strategies cooked up elsewhere in the organization. The phrase, “make it pretty,” best captures this ethos.

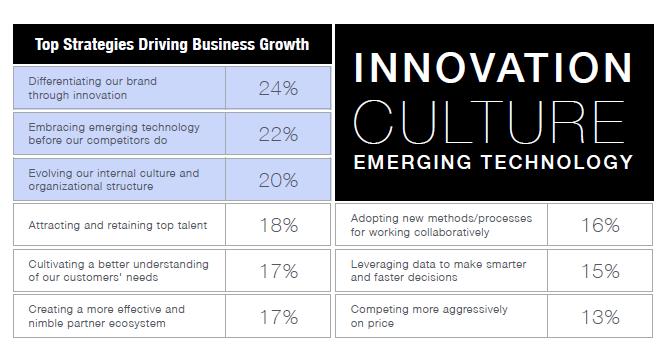

But times are changing, and design leaders increasingly find themselves at the helm of successful start-ups, in advisory capacities at VC firms, or in newly minted C-level roles at traditional brands. John Maeda first reported on this trend in his annual “Design in Tech” report and our Global Digital Outlook Study adds further proof. This year, 67% of business executives agreed that creative and design leaders were having a bigger impact on the overall strategic direction of their business. Furthermore, they pointed to “brand differentiation through innovation” and “adopting emerging technology before our competitors do” as the most important strategic factors driving business success over the next two years.

This is welcome news for creative agencies hungry for allies in the executive suite. But more support in the C-suite won’t necessarily translate into easier wins. For starters, client-side leaders continue to elevate their expectations for agency partners. In fact, “Better Design/Creative” is the top attribute clients would like to see more of in their agency partners…. even ahead of criteria such “more flexible working models,” “stronger data capabilities,” “stronger technology capabilities” and more. Translation? No free rides on the creative front. 70% of client-side leaders also admitted that quantifying and valuing the business impact of creative/design ideas presents an increasing challenge for how they compensate their agency partners. The bottom line: creative and design leaders are on the rise in corporate structures and there’s no doubt that this can help bolster the influence of creative agencies in the board room. But increased visibility leads to increased scrutiny… for the caliber of the creative work product and, more importantly, the direct business value it creates. Agency leaders have their work cut out for them.

6. DIGITAL PRODUCT STUDIOS POISED FOR GROWTH

Of all the data we track, one trend that continues to stick out is the growing focus— for both client-side marketers AND agency leaders— on the creation, design and development of new digital products and services distinctive from traditional creative work on marketing-related content, campaigns and experiences.

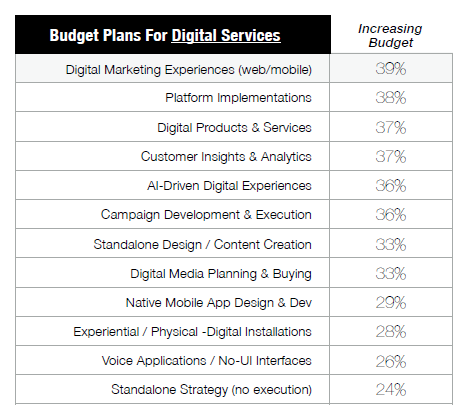

45% of agency leaders this year projected that revenue related to helping their clients create, launch and improve digital products and services would increase in 2019. This was the top-ranked category for agency revenue growth (tied with Customer Insights & Analytics) even though just 9% of agency respondents identified themselves as “Digital Product Design Studios.” 42% of agency leaders also pointed to “more consulting with clients on new product and service offerings” as the one of the major ways in which their engagement models have been changing… the top-ranked attribute in this category. In fact, the digital product and service trend is most striking among those identifying as “Digital Agencies.” 65% of this segment anticipate increased revenue for digital product work in 2019 and 60% report this as a major change to their typical engagement models.

7. EMERGING TECHNOLOGY IS, WELL, STILL EMERGING

New technologies come to market at a rapid pace and each one of them challenges business leaders and agencies with the choice of where to experiment, where to invest and where to wait and see. AI technology and initiatives related to AI-driven digital experiences were top of mind this year. Collectively, 56% agreed that “AI technology will significantly impact the way we plan for and design customer interactions.” 36% of marketing leaders plan to increase spending for “AI-Driven Digital Experiences” in 2019 and 36% describe their investment levels in this area as “significant.” But it’s still early days. Just 16% of respondents said they are actively working on AI-related projects and 27% have no plans to tackle AI in the next 12 months. The remaining 57% have just begun to explore the technology or plan to begin their first initiatives in 2019.

Outside of AI, we steady adoption for technologies related to AR/VR/Mixed Reality, voice-based experiences and even blockchain. More than one-third of marketers are planning “significant investments” in these areas in 2019. The broader domain of “Marketing Automation” topped the list of emerging technologies in terms of anticipated spending and impact. Marketing leaders and agency leaders identified it as the top area for investment (46% of client-side marketers plan to make “significant investments” in 2019), and potential impact (37% of agency leaders anticipate that marketing automation will have a “significant impact” on their client’s marketing approaches in the next 12 months). While Marketing Automation, as a category, encompasses other emerging technologies (particularly AI), it’s clear that business leaders are prioritizing technology investments into solutions that can help

alleviate key pressure points such as speed, scale, efficiency and effectiveness.

Here some other interesting facts from the report:

You can download the report here: http://sodareport.com/forecast/research-findings/

About the author: Tom Beck is Executive Director of SoDA and works closely with its membership, Board of Directors and corporate partners to create an indispensable global network for digital business leaders, creative visionaries and technology disruptors.

2 thoughts on “Forrester & SoDA Global Digital Outlook 2019”

Comments are closed.